Construction project should be:

- a new development or expansion of an existing facility

- have a minimum of $25 million and a maximum of $500 million Canadian dollars in eligible capital costs

- employ over 250 personnel during construction or employ 15+ skilled workers (job that requires a degree, certificate, or trade credential)

- support natural resources extraction

- not be linear property as defined by the Municipal Government Act

- commence construction after this bylaw comes into effect.

Property requirements

To be considered for a Tax Incentive Agreement, the property or development project must fulfill the following requirements:

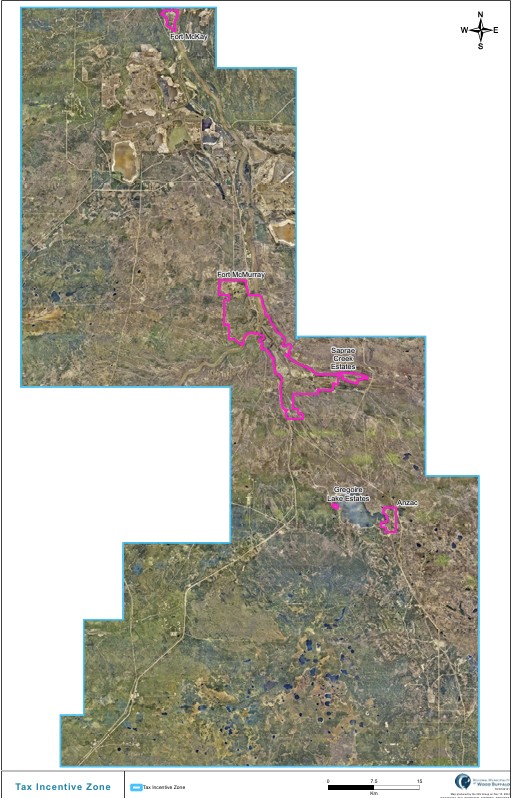

- be situated within the Tax Incentive Zone

- obtain all the necessary development approvals

- comply with all the terms of the development agreement and the Safety Code Act during the agreement period and not face any foreclosure or violation.

Applicant Requirements:

- must be the Assessed Person or have authorization from the Assessed Person

- must not have any outstanding debts or amounts owed to the Municipality

- should not be undergoing bankruptcy or receivership

- must adhere to the terms and conditions of any grant or other financial assistance received from the Municipality,

- should not be engaged in any legal disputes against the Municipality.

{kind=link}